Fill in a Valid St 7 New Jersey Template

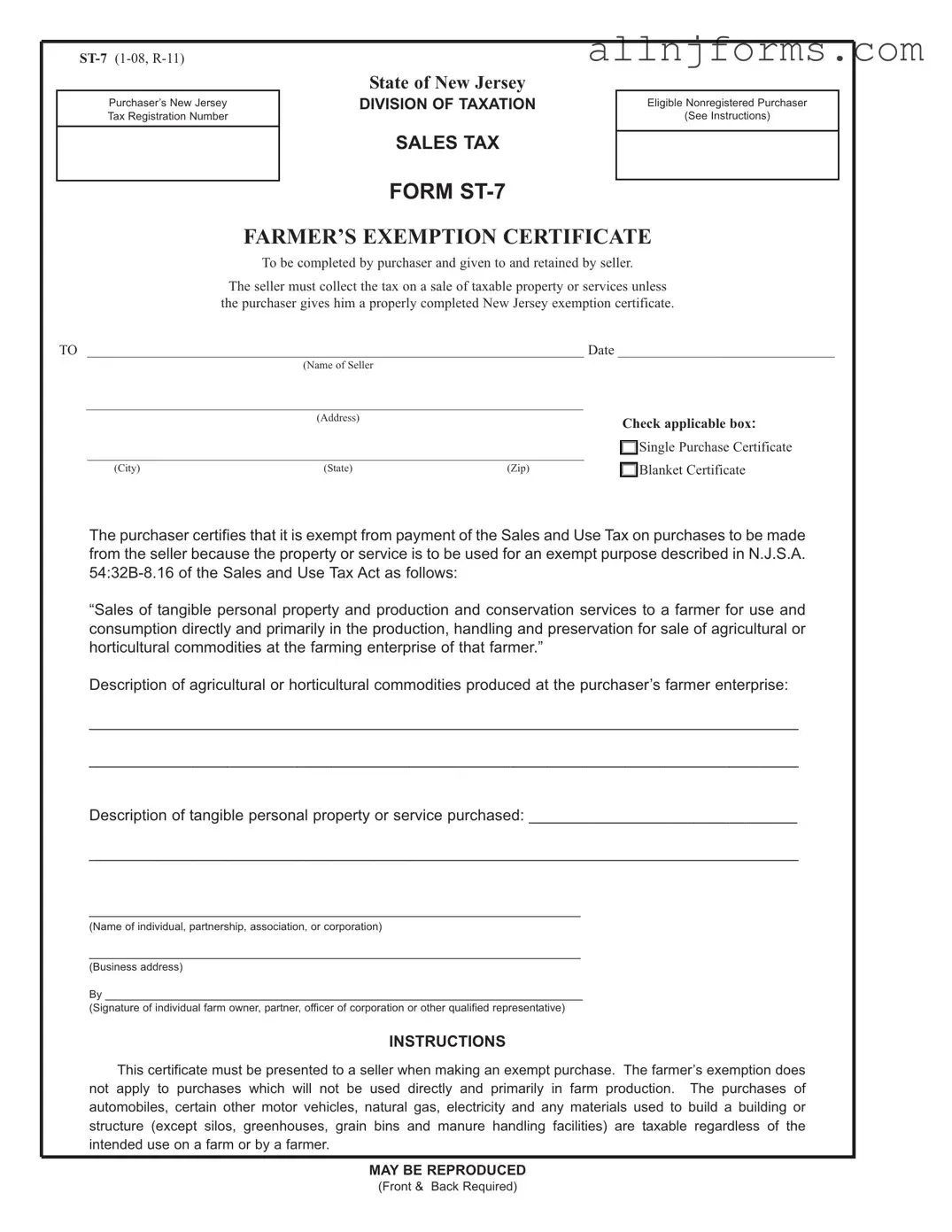

The ST-7 form, also known as the Farmer’s Exemption Certificate, is a crucial document for farmers in New Jersey who wish to make tax-exempt purchases related to their agricultural activities. This form serves as a declaration that the purchaser is exempt from sales tax on certain items used directly in farming operations. It is essential for sellers to collect sales tax unless they receive a properly completed ST-7 form from the purchaser. The form must include specific information, such as the seller's name and address, as well as details about the agricultural commodities produced and the tangible personal property or services being purchased. Farmers must understand that this exemption applies only to items that will be used primarily in agricultural production, which excludes purchases like vehicles and certain utilities. Additionally, the ST-7 form must be presented at the time of purchase, and sellers are required to retain these certificates for a minimum of four years to comply with tax regulations. Understanding the nuances of this form is vital for both farmers and sellers to ensure compliance and avoid potential tax liabilities.

Example - St 7 New Jersey Form

Purchaser’s New Jersey Tax Registration Number

State of New Jersey

DIVISION OF TAXATION

SALES TAX

FORM

Eligible Nonregistered Purchaser

(See Instructions)

FARMER’S EXEMPTION CERTIFICATE

To be completed by purchaser and given to and retained by seller.

The seller must collect the tax on a sale of taxable property or services unless the purchaser gives him a properly completed New Jersey exemption certificate.

TO _______________________________________________________________________ Date _______________________________

(Name of Seller

_______________________________________________________________________

|

(Address) |

|

Check applicable box: |

|

|

|

|

||

_______________________________________________________________________ |

|

Single Purchase Certificate |

||

|

||||

|

|

|||

(City) |

(State) |

(Zip) |

|

Blanket Certificate |

ThepurchasercertifiesthatitisexemptfrompaymentoftheSalesandUseTaxonpurchasestobemade from the seller because the property or service is to be used for an exempt purpose described in N.J.S.A.

“Sales of tangible personal property and production and conservation services to a farmer for use and consumption directly and primarily in the production, handling and preservation for sale of agricultural or horticultural commodities at the farming enterprise of that farmer.”

Description of agricultural or horticultural commodities produced at the purchaser’s farmer enterprise:

__________________________________________________________________________________

__________________________________________________________________________________

Description of tangible personal property or service purchased: _______________________________

__________________________________________________________________________________

_______________________________________________________________________

(Name of individual, partnership, association, or corporation)

_______________________________________________________________________

(Business address)

By _____________________________________________________________________

(Signature of individual farm owner, partner, officer of corporation or other qualified representative)

INSTRUCTIONS

This certificate must be presented to a seller when making an exempt purchase. The farmer’s exemption does not apply to purchases which will not be used directly and primarily in farm production. The purchases of automobiles, certain other motor vehicles, natural gas, electricity and any materials used to build a building or structure (except silos, greenhouses, grain bins and manure handling facilities) are taxable regardless of the intended use on a farm or by a farmer.

MAYBE REPRODUCED

(Front & Back Required)

INSTRUCTIONS FOR USE OFFARMER’S EXEMPTION CERTIFICATE

1.

NOTE: For sales and use tax purposes, a “farming enterprise” does not include an enterprise that is primarily engaged in boarding or training horses or in selling agricultural or horticultural products produced by others.

The farmer’s exemption applies only to sales of tangible personal property or services which will be used directly and primarily in agricultural or horticultural production. It does not apply to sales of: motor vehicles, natural gas, electricity, or property to be used to construct a building or structure (with the exception of silos, greenhouses, grain bins, or manure handling facilities).

NOTE: Whenpurchasingatruckortrucktractorwithagrossvehicleweightratingofmorethan18,000poundswhichisregisteredwith the New Jersey Division of Motor Vehicles as a farm vehicle or a commercial

2.Good Faith- To act in good faith means to act in accordance with standards of honesty. In general, registered sellers who accept exemption certificates in good faith are relieved of liability for the collection and payment of sales tax on the transaction covered by the exemption certificate.

In order for good faith to be established, the following conditions must be met:

(a)Certificate must contain no statement or entry which the seller knows is false or misleading;

(b)Certificate must be an official form or a proper and substantive reproduction, including electronic;

(c)Certificate must be filled out completely;

(d)Certificate must be dated and include the purchaser’s New Jersey tax identification number or, for a purchaser that is not registered in New Jersey, the Federal employer identification number or

(e)Certificate or required data must be provided within 90 days of the sale.

The seller may, therefore, accept this certificate in good faith as a basis for exempting sales to the signatory purchaser and is relieved of liability even if it is determined that the purchaser improperly claimed the exemption.

3.Blanket Certificates - Aseller may permit a purchaser to file a blanket Farmer’s Exemption Certificate to cover future purchases of similar items of tangible personal property. However, each subsequent sales slip or purchase invoice based on such blanket certificate must be clearly marked with the purchaser’s name, address, and identification number.

4.Eligible Nonregistered Purchaser - If the purchaser is not required to be registered with the New Jersey Division ofTaxation and does not have a New Jersey Tax Registration Number, the purchaser is required to place either his Federal Identification Number or, if a sole proprietor, the last three digits of his Social Security Number in the box at the top, right corner of the form marked “Eligible NonregisteredPurchaser.” Note: AnyNewJerseyfarmerwhoisnotasoleproprietor,orwhosellsanygoodsorservicessubjecttosales tax, or who is an employer, must be registered with the New Jersey Division of Taxation and therefore cannot be an “eligible nonregistered purchaser”.

5.

6.Retention of Certificates - Certificates must be retained by the seller for a period of not less than four years from the date of the sale covered by the certificate.

REPRODUCTION OFFARMER’S EXEMPTION CERTIFICATES:

Private reproduction of both sides of these certificates may be made without the prior permission of the Division of Taxation

FOR MORE INFORMATION:

Call the Customer Service Center (609)

Form Specs

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The ST-7 form is a Farmer’s Exemption Certificate used in New Jersey to certify that a purchaser is exempt from sales tax for certain agricultural purchases. |

| Governing Law | The form is governed by N.J.S.A. 54:32B-8.16 of the Sales and Use Tax Act. |

| Eligibility | This certificate can only be used by businesses classified as “farming enterprises” under state law. |

| Exempt Purchases | Exempt purchases include tangible personal property and services used directly in agricultural production. |

| Non-Eligible Items | Items such as motor vehicles, natural gas, and electricity are not eligible for exemption under this form. |

| Good Faith Requirement | Sellers must act in good faith when accepting the ST-7 form to be relieved of tax liability. |

| Certificate Retention | Sellers must keep the completed certificates for at least four years from the date of the sale. |

| Blanket Certificates | A blanket certificate can be filed for future similar purchases, but each transaction must be documented properly. |

| Nonregistered Purchasers | Nonregistered purchasers must provide their Federal Identification Number or Social Security Number on the form. |

| Improper Certificate Consequences | Sales not supported by a properly executed certificate are considered taxable, and the seller bears the burden of proof. |

More PDF Documents

Transfer Tax Nj - For those involved in a real estate transaction in New Jersey, the RTF-1 form is a mandatory document that outlines the financial specifics of the deal for tax purposes.

Njdep Opra - It acts as a requisition form for public or private individuals seeking reports from New Jersey state.

For anyone needing a financial solution, our guide to the Maryland Promissory Note form is invaluable. This document helps clarify the terms of the loan agreement, ensuring both parties are aligned on repayment terms and conditions. To begin, access the essential resources for creating your Promissory Note template today.

How to Become a Private Investigator in Nj - Selecting two potential names for the detective agency is necessary for the authorization process.